UK Pea Protein Industry Outlook: Trends, Forecasts & Growth Drivers (2025–2032)

United Kingdom Pea Protein Market Analysis: Growth Landscape, Trends, and Future Outlook

The United Kingdom Pea Protein Market is expanding steadily as plant‑based nutrition gains traction among consumers seeking health‑oriented and sustainable food options. According to industry estimates, the market was valued at approximately USD 302.30 million in 2024 and is projected to reach around USD 419.81 million by 2032, growing at a compound annual growth rate (CAGR) of about 4.19 percent during the forecast period. This growth reflects a broader shift in dietary preferences, increasing vegan and flexitarian populations, and rising reformulation of food products to include high‑quality plant proteins in mainstream and specialty foods.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/United

Market Estimation & Definition

Pea protein refers to protein extracted from legumes such as yellow split peas, chickpeas, and lentils, valued for its nutritional strengths, functional performance, and hypoallergenic properties. It provides a high‑quality plant protein source, with an amino acid profile that supports muscle health while being free from common allergens such as soy and dairy. Pea protein’s functional characteristics — including emulsification, water binding, foaming, and gelation — make it suitable for a wide range of food and beverage formulations. Within the UK market, pea protein is used in meat alternatives, nutritional supplements, beverages, and snacks, increasingly replacing traditional proteins in both retail and foodservice products.

Market Growth Drivers & Opportunity

Evolving Consumer Lifestyles: One of the major factors driving the growth of the pea protein market in the United Kingdom is the rise of plant‑based diets and health‑conscious consumption. An increasing number of UK consumers are adopting vegan, vegetarian, or flexitarian lifestyles, motivated by concerns about personal health, animal welfare, and environmental sustainability. This trend is translating into higher demand for plant‑derived proteins that deliver nutritional value and align with lifestyle choices.

Environmental Sustainability Trends: Increasing awareness about the environmental impact of food production has spurred interest in plant‑based proteins, including pea protein. Pea cultivation typically requires fewer resources such as water and land compared to animal protein production, and has a lower carbon footprint, making it an attractive ingredient for sustainability‑focused food brands and consumers. These environmental benefits are resonating strongly with UK buyers and increasing plant‑based adoption.

Food Reformulation Across Categories: UK food manufacturers are actively reformulating products to meet consumer demand for higher protein content, clean‑label ingredients, and allergen‑free formulations. This has encouraged the inclusion of pea protein in products ranging from meat analogues and beverages to fortified snacks and nutrition bars. Growth in the sports and health nutrition sector also supports use of pea protein as a key ingredient in protein powders and supplements aimed at fitness‑oriented consumers.

Despite these opportunities, the market faces challenges related to the higher production costs of pea protein compared with some conventional proteins and supply chain dynamics typical of commodity‑based markets. Addressing these issues through innovation and strategic alliances across the supply chain could unlock further growth potential.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/United

What Lies Ahead: Emerging Trends Shaping the Future

Innovation in Processing and Functionality: Advances in protein extraction and formulation technologies are improving the functional attributes of pea protein, making it easier to incorporate into diverse food products without compromising taste, texture, or nutritional value. These improvements are expanding the range of applications for pea protein in both mainstream and specialized products.

Clean‑Label and Allergen‑Free Positioning: UK consumers are increasingly discerning about ingredient lists and are gravitating toward products with simple, transparent formulations. Pea protein’s profile as a clean‑label, allergen‑friendly ingredient enhances its appeal in both retail and foodservice markets.

Cross‑Sector Applications: While food and beverage applications remain dominant, pea protein is also gaining ground in adjacent segments such as animal feed, nutraceuticals, and personal care products. These lateral applications are broadening the UK market base and introducing new revenue streams for producers and ingredient suppliers.

Segmentation Analysis

The UK pea protein market can be segmented by product type, form, source, and application. Protein isolates currently hold a significant share, driven by their high protein content and functional versatility in various formulations. Protein concentrates and textured pea protein also contribute to the market, particularly in applications requiring structural or sensory properties commonly used in meat alternatives.

In terms of form, dry pea protein dominates due to ease of storage and incorporation into food products, whereas wet forms are used in certain specialized beverage and ready‑to‑drink applications.

The source segment includes ingredients derived from yellow split peas, chickpeas, and lentils, with yellow split peas being the most prevalent due to their availability and yield efficiency.

By application, the market spans food and beverages, meat extenders and substitutes, sports nutrition products, snacks, beverages, and nutritional supplements. Food and beverage applications represent the largest share, reflecting broad adoption of pea protein across multiple consumer categories.

Country Level Analysis

The United Kingdom’s pea protein market growth is strongly influenced by urban consumption patterns and evolving dietary preferences. Urban centers such as London, Manchester, Edinburgh, and Birmingham are key hubs of demand, driven by high concentrations of health‑oriented consumers and robust food manufacturing activity. Retailers in these regions are increasingly stocking plant‑based protein products, further supporting market expansion.

Government policies encouraging sustainable food systems and reduced meat consumption also contribute to favorable conditions for plant‑based proteins in the UK, aligning public health goals with market development.

Competitor Landscape

The competitive environment for pea protein in the United Kingdom includes established ingredient producers and specialty manufacturers such as Nutri‑Pea Limited, Roquette Frères, and Farbest Brands. These companies focus on capacity expansion, product innovation, and partnership with food manufacturers to strengthen their market positions.

Press Release Conclusion

In summary, the United Kingdom Pea Protein Market is poised for sustained growth through 2032, driven by rising consumer interest in plant‑based diets, sustainability imperatives, and expanding applications across food and nutrition categories. With ongoing innovation in product technology and formulation, increasing acceptance of pea protein in mainstream food systems, and supportive regulatory environments, this market is set to play a central role in the UK’s transition toward healthier and more sustainable protein sources.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Top Healthy Food Trends Shaping the Nutraceutical Landscape (2025–2032)

Smart Door Lock Market Analysis: Growth, Opportunities, and Future Outlook

The global Smart Door Lock Market is undergoing a transformative phase, as technologies that once belonged to high-end luxury homes have become mainstream in both residential and commercial environments. Fueled by the convergence of digital connectivity, rising security concerns, and the rapid adoption of smart home ecosystems, smart door locks are setting a new standard in access control and convenience. According to the latest industry intelligence, this market was valued at USD 2.78 billion in 2024 and is forecast to surge to USD 11.66 billion by 2032, expanding at a CAGR of approximately 19.6% through the forecast period.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/Smart-

Market Estimation & Definition

The smart door lock market encompasses digitally enabled access control systems that replace or augment traditional mechanical locks with advanced technologies such as Bluetooth, Wi-Fi, biometrics, and mobile-app-based controls. These products provide not only heightened security but also remote control features, user authentication, and integration with broader smart home environments. Unlike conventional locks, smart door locks allow users to grant access through encrypted codes, digital key cards or smartphones, offering flexibility and real-time monitoring capabilities.

This market’s rapid expansion is driven by rising demand for connected home solutions, heightened consumer awareness of the benefits of automation, and increasing urbanization in developing economies. Additionally, growing e-commerce and package delivery services have amplified the need for secure, hassle-free delivery access — further propelling the adoption of smart access systems.

Market Growth Drivers & Opportunity

Several powerful forces are fueling growth in the smart door lock market:

Smart Home Integration: The proliferation of Internet of Things (IoT) devices and seamless connectivity with smartphones and voice assistants have made smart locks fundamental components of modern home automation systems.

Security and Convenience: Consumers are increasingly prioritizing security features such as remote monitoring, tamper alerts, and temporary access codes for guests or service personnel. These features set smart door locks apart from traditional locking mechanisms in both convenience and functionality.

Rising E-commerce and Delivery Needs: With online shopping on the rise, secure package delivery has become a priority. Smart locks offer secure entry for couriers during predefined delivery windows, reducing theft risk.

Energy Efficiency & Sustainability: Some smart door lock systems incorporate energy-saving automation, such as proximity-based locking, appealing to environmentally conscious consumers.

Strategic Partnerships and Integration: Collaborations between smart lock makers and home security providers, telecom operators, and service platforms represent untapped value creation opportunities.

These drivers are compounded by continuing innovation in encryption, biometric authentication, and AI-enabled usage analytics, creating strong product differentiation potential.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/Smart-

What Lies Ahead: Emerging Trends Shaping the Future

As the smart door lock market matures, several trends are emerging that will shape its evolution:

DIY Installations: Growing consumer preference for do-it-yourself setups has expanded market reach by reducing installation barriers.

Enhanced Security Protocols: Future product generations will integrate advanced threat detection, biometric verification, and machine learning for behavior-based access controls.

Smart Home Ecosystem Compatibility: Interoperability with voice assistants and smart home hubs is becoming a must-have, enabling voice activation and centralized system management.

Localized Services: Tailored solutions for sectors such as hospitality, commercial buildings, and multi-unit residential complexes will diversify demand.

These trends suggest a future where smart door locks are not only secure entry systems but also intelligent nodes within larger connected property ecosystems.

Segmentation Analysis

The smart door lock market is examined across several key dimensions:

Product Type: Includes keyless entry systems featuring PIN, voice commands, or biometrics; Bluetooth-enabled locks; Wi-Fi connected locks; Zigbee protocol devices; and hybrid mechanical-electronic units.

End-User: Residential users dominate due to heightened demand for smart homes, while commercial users seek enhanced access control solutions.

Price Range: Products range from budget-friendly basic models to mid-range offerings and premium locks with advanced features.

Installation Type: DIY installable units appeal to mainstream consumers, whereas professional installation is preferred for enterprise and high-security environments.

Protection Level: Basic models provide essential access control, whereas advanced locks deploy encryption, biometrics, and intrusion detection.

Country Level Analysis

Among regions, North America holds a dominant position with around 39% market share, primarily driven by the United States’ robust smart home adoption and high consumer spending power. This trend is expected to continue as more U.S. households adopt smart security solutions in response to rising safety concerns.

In Germany, the broader European embrace of smart home technologies — supported by energy-efficient housing initiatives — is stimulating steady demand in both residential and commercial segments.

Across other regions, Asia Pacific is projected to exhibit rapid growth, led by urban development, smart city initiatives, and increasing technology penetration in markets like India and China.

Competitive Landscape

Market competition is intense, with established players offering a range of innovative solutions. Leading manufacturers include ASSA ABLOY, Kwikset, Yale Locks, Honeywell, and Samsung SDS among others. These companies are investing in product enhancements, integration capabilities, and cybersecurity features to strengthen market positions.

Press Release Conclusion

In summary, the Smart Door Lock Market is set for robust growth through 2032, driven by technological innovation, rising security awareness, and the increasing popularity of connected home ecosystems. With multiple segments offering diverse opportunities, companies that successfully combine security, convenience, and interoperability will lead the next wave of market expansion.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Range Cooker Market: Combining Tradition and Innovation in Modern Kitchens

The Range Cooker Market — encompassing freestanding kitchen appliances that integrate ovens and hobs into a single unit — is on a strong global growth trajectory as consumers and commercial kitchens increasingly prefer high-performance, multifunctional cooking solutions. According to Stellar Market Research, the global range cooker market was valued at approximately USD 1.73 billion in 2024 and is projected to reach around USD 3.16 billion by 2032, growing at a compound annual growth rate (CAGR) of about 7.8 % over the forecast period.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/Range-

Market Estimation & Definition

A range cooker is a freestanding kitchen appliance that combines multiple cooking functions — including baking, roasting, grilling and simmering — in one unit, typically offering larger capacities and additional burners when compared to standard ovens or cooktops. These appliances are available in various styles and fuel types — such as electric, gas and induction — catering to diverse consumer requirements. Range cookers also often feature integrated storage spaces for cookware and offer aesthetic versatility with design options suited to both contemporary and traditional kitchens.

Range cookers are widely used in residential kitchens for everyday cooking and in commercial settings such as restaurants and catering services where flexibility and capacity are essential. They appeal to consumers seeking performance, convenience and kitchen aesthetics, with modern models increasingly incorporating energy-efficient operation and smart features.

Market Growth Drivers & Opportunity

Rising Consumer Demand for Multifunctionality: Modern consumers prefer appliances that deliver multiple cooking modes in one unit, reducing the need for separate ovens or cooktops. Range cookers meet this demand by offering versatility and convenience — from baking and roasting to simmering and grilling — in a single appliance.

Urbanization and Growing Middle-Class Population: Rapid urbanization and the expanding middle-class segment in emerging economies are increasing disposable incomes and driving investment in home improvement and kitchen upgrades. As households seek premium, efficient kitchen appliances, range cooker sales continue to rise.

Home Cooking Trends: There has been a global shift toward home cooking, led by lifestyle changes and increased health consciousness. Range cookers — with their larger capacities and multifunctional design — are now seen as practical investments for enthusiasts and everyday chefs alike.

Technological Innovation: Manufacturers are integrating advanced features such as smart controls, induction heating, Wi-Fi connectivity and energy-efficient systems, appealing to tech-savvy consumers who want convenience and control.

Kitchen Remodeling and Aesthetics: Range cookers are increasingly featured as centerpiece appliances in open plan and luxury kitchen designs, supported by strong interior design trends and renovation activity that emphasize both functionality and visual appeal.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/Range-

What Lies Ahead: Emerging Trends Shaping the Future

Smart and Connected Appliances: Range cookers with smart connectivity — enabling remote control, app-based settings and voice assistant integration — are gaining traction, enhancing user convenience and aligning with broader smart home ecosystems.

Energy Efficiency Focus: Energy-efficient range cookers — especially induction models and those complying with evolving global efficiency standards — are becoming more desirable as consumers and regulators prioritize sustainability.

Customized and Premium Offerings: Premium models with dual-fuel capabilities, large oven capacities, designer finishes and customizable features are attracting affluent buyers and cooking enthusiasts seeking stylistic and performance enhancements.

Expansion in Emerging Markets: Rapid urbanization and rising kitchen renovation activity in Asia-Pacific, Latin America and the Middle East are driving demand for range cookers in regions where modern kitchen appliances were historically underpenetrated.

Segmentation Analysis from the Report

According to the Stellar Market Research report, the range cooker market is segmented by key dimensions:

By Type:

Electric range cookers

Gas range cookers

Induction range cookers

By Price Range:

Premium range

Mid-range

Economy

By Distribution Channel:

Offline (specialty stores, retail outlets)

Online (e-commerce platforms)

By Application:

Residential — dominated by home kitchens and renovation projects

Commercial — includes restaurants, hotels, catering and institutional kitchens

Industrial — large-scale facilities with high-capacity cooking needs

This segmentation reveals how product type, pricing strategy, distribution reach and application scenarios define demand patterns and growth opportunities across global markets.

Country-Level Analysis: USA and Germany

United States: The U.S. range cooker market remains strong, supported by high consumer spending on premium kitchen appliances and robust home remodeling trends. Growing interest in gourmet cooking and professional-grade appliances further fuels demand for larger, multifunctional range cookers in residential settings.

Germany: Germany — being a significant European home appliance market — demonstrates steady demand for energy-efficient and advanced range cookers. European sustainability standards and design preferences support the adoption of efficient, connected range cookers, while commercial adoption in hospitality settings also bolsters sales in this market.

Both markets reflect broader regional trends where upgrading kitchen infrastructure and embracing advanced appliance technology are core drivers for range cooker adoption.

Commutator Analysis (Competitive Landscape)

The global range cooker market features major appliance manufacturers competing on product innovation, energy efficiency, brand reputation and distribution strength. Key companies include:

Electrolux

Bosch

Whirlpool

Haier

Miele

Aga Rangemaster Group

Sub-Zero Group

LG Electronics

Samsung Electronics

Fisher & Paykel

Bertazzoni

Viking Range

JennAir

Dacor

Thermador

Smeg

Gorenje

Siemens

AEG

Zanussi

Baumatic

Neff

Candy

Hoover

Beko

These companies focus on expanding product portfolios, incorporating smart features, enhancing energy performance, and strengthening distribution networks to capture evolving customer preferences and geographic demand.

Press Release Conclusion

The Range Cooker Market is set for robust growth through 2032, propelled by rising demand for multifunctional cooking solutions, expanding smart appliance adoption and growing investment in home renovation and kitchen upgrades. With a projected rise from around USD 1.73 billion in 2024 to approximately USD 3.16 billion by 2032 at a healthy CAGR of about 7.8 %, the market reflects evolving consumer preferences for performance, convenience, energy efficiency and design excellence. As manufacturers innovate with connected features, energy-efficient technologies and premium products — and as major markets like the United States and Germany continue to invest in advanced kitchen appliances — range cookers will remain central to modern culinary lifestyles and commercial applications worldwide.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Leisure Rentals to Grow Fastest — Luxury Cars for Vacations, Weddings & Special Occasions

Luxury Car Rental Market: Driving Luxury Mobility with Premium Experiences

The Luxury Car Rental Market is witnessing steady global growth as consumers increasingly prefer premium mobility solutions for business travel, leisure experiences, and special events. According to Stellar Market Research, the global luxury car rental market was valued at approximately USD 57.76 billion in 2024 and is estimated to grow at a compound annual growth rate (CAGR) of about 5.5 % from 2025 to 2032, reaching USD 88.64 billion by 2032. (turn0search0; turn0search2)

Luxury car rentals — which provide high‑end vehicles such as premium sedans, SUVs, and exotic marques for short‑ or long‑term use — cater to affluent consumers, corporate clients, and travelers seeking superior comfort, performance, and prestige without the cost and commitment of ownership.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/luxury

Market Estimation & Definition

A luxury car rental service offers access to high‑performance, high‑comfort vehicles from renowned brands such as Mercedes‑Benz, BMW, Audi, Porsche, and Rolls‑Royce for flexible periods, often ranging from hours to weeks. These rentals are used for executive travel, holidays, airport transport, weddings, VIP events, and experiential leisure journeys. The infrastructure supporting luxury rentals includes both online booking platforms and traditional offline rental desks at airports, city hubs, and upscale hotels. (turn0search

This market segment has evolved beyond traditional rental agencies as digitalization allows customers to review, select, and reserve luxury vehicles online with real‑time availability, pricing comparisons, and personalized service options. (turn0search

Market Growth Drivers & Opportunity

Several core factors are driving the luxury car rental market:

1. Rising Disposable Incomes & Premium Travel Demand

Growing disposable incomes, increased international travel, and the expanding global affluent population are elevating demand for high‑end experiences, including luxury vehicle rentals during trips and events. Consumers — especially millennials and Gen Z — increasingly choose experience‑based mobility over ownership. (turn0search2)

2. Business Mobility Requirements

Luxury rentals serve a crucial role in corporate mobility, conference travel, executive engagements, and incentive travel programs. Businesses are opting for premium rentals for comfort, status, and productivity on the road without adding capital assets to their balance sheets. (turn0search

3. Digitization & Online Booking Adoption

Online reservations dominate the booking landscape, capturing a significant share as customers prefer the convenience of comparing luxury vehicle inventory, pricing, and features before confirming a rental. Young, tech‑savvy consumers and frequent travelers drive this shift globally. (turn0search

4. Experiential and Tourism‑Led Travel Trends

Luxury car rentals are bundled with high‑end tourism packages, luxury hotel experiences, and travel events, making them part of broader luxury lifestyles rather than just transport solutions — a trend that continues to expand market opportunities. (turn0search2)

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/luxury

What Lies Ahead: Emerging Trends Shaping the Future

Shift Toward Electric & Hybrid Luxury Fleets

Sustainability concerns and stricter emission norms are prompting rental companies to integrate electric and hybrid luxury vehicles into their fleets. This supports eco‑luxury travel and aligns with corporate ESG priorities. (turn0search2)

AI and Smart Fleet Management

Rental firms are deploying artificial intelligence and machine learning for predictive maintenance, automated fleet allocation, and enhanced customer experience — including customized recommendations, dynamic pricing, and loyalty programs. (turn0search2)

Subscription & Long‑Term Rental Models

Subscription services are emerging as a premium alternative to short‑term rentals, allowing customers to access a variety of luxury vehicles on flexible monthly plans without long‑term ownership costs. Industry data suggests these subscription trends are gaining traction as consumer preferences shift toward convenience and variety. (turn0search8)

Special Events and Concierge Services

High‑end concierge and chauffeur services bundled with luxury rentals are attracting affluent travelers for weddings, galas, and exclusive cultural events, adding new revenue streams for providers.

Segmentation Analysis from the Report

According to Stellar Market Research, the luxury car rental market is segmented by rental type and mode of booking: (turn0search

By Rental Type:

Business Rental — Dominated the market with 57 % share in 2024, driven by corporate leasing programs, executive travel, and business conference transport needs.

Leisure Rental — Expected to grow rapidly as consumers prefer luxury experiences for vacations, celebrations, and high‑end travel.

By Mode of Booking:

Online Booking — Held the largest share (56 % in 2024) as customers increasingly prefer digital reservation systems.

Offline Booking — Still relevant in established markets through traditional rental desks, particularly at airports and physical branches.

These segmentation bases reflect how business demand currently drives revenue, while leisure and digital convenience are key growth accelerators.

Country Level Analysis: USA and Germany

United States:

The U.S. luxury car rental market benefits from a mature travel and mobility ecosystem, with strong corporate mobility demand, affluent domestic and international tourism, and high digital adoption rates. Airport rentals and online booking platforms lead service delivery, supported by established rental brands and premium travel hubs.

Germany:

In Europe, Germany is a significant luxury rental market due to a robust automotive heritage, high GDP per capita, and strong tourism demand. Key cities serve as hubs for premium travel experiences and business visitors, driving consistent rental utilization rates. Online reservations and integrated mobility services (such as app‑based bookings) are increasingly prominent.

Commutator Analysis (Competitive Landscape)

The luxury car rental market features a mix of global rental giants and regional players with diverse fleet offerings and service models: (turn0search

Avis Budget Group (U.S.)

Goldcar (Spain)

Sixt (Germany)

Enterprise Holdings (U.S.)

Movida (Brazil)

Fox Rent a Car (U.S.)

Hertz (U.S.)

Localiza (Brazil)

Unidas (U.S.)

eHi Car Services (China)

These companies compete through fleet diversity, digital platforms, airport presence, customer service, and strategic partnerships with airlines, hotels, and travel agencies to capture premium market share and enhance global reach.

Press Release Conclusion

The Luxury Car Rental Market is set for sustained expansion through 2032, rising from approximately USD 57.76 billion in 2024 to about USD 88.64 billion at a CAGR of 5.5 %, driven by business travel demand, leisure experiences, and digital booking adoption. Integrating electric and hybrid luxury vehicles, expanding subscription models, and smart fleet technologies will further shape the future of luxury car rentals. With strong performance in key markets like the United States and Germany, the sector is evolving from conventional rentals into an experience‑driven, technology‑enhanced premium mobility ecosystem.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com

Why UPS Batteries Are Critical in a Rapidly Digitizing World

UPS Battery Market: Powering Reliability and Continuity Across Industries

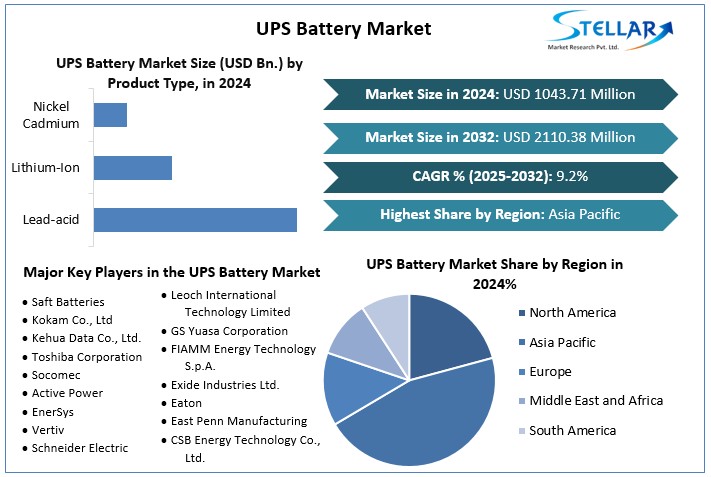

The Uninterruptible Power Supply (UPS) Battery Market plays a crucial role in ensuring reliable power backup for critical systems across residential, commercial, industrial, and data center applications. UPS batteries serve as essential components that provide emergency power during utility outages, protect sensitive equipment from voltage fluctuations and surges, and enable graceful system shutdowns to prevent data loss and equipment damage. According to the latest Stellar Market Research analysis, the global UPS battery market was valued at around USD 1,043.71 million in 2024 and is expected to reach approximately USD 2,110.38 million by 2032, growing at a compound annual growth rate (CAGR) of about 9.2 % from 2025 to 2032.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/UPS-Ba

Market Estimation & Definition

A UPS battery is a rechargeable energy storage system integrated with uninterruptible power supply systems that provide temporary power during utility failures or instabilities. These batteries — typically lead-acid, lithium-ion, or nickel-cadmium — ensure that connected devices such as servers, telecommunications equipment, industrial machines, and residential electronics continue to operate seamlessly until alternative power sources or generators take over. They are indispensable in sectors where uptime is critical and even short power interruptions can lead to significant losses.

Market Growth Drivers & Opportunity

Several key factors are driving growth in the UPS battery market:

Rising Demand for Reliable Backup Power: As businesses increasingly rely on digital infrastructures such as data servers, cloud computing, and automated processes, the need for uninterrupted power has become mission-critical. UPS batteries provide essential protection against power interruptions that could otherwise lead to data loss, operational delays, or equipment damage.

Expansion of Data Centers and Cloud Services: The proliferation of data centers, edge computing facilities, and cloud service infrastructure has significantly boosted UPS battery demand. These facilities require robust power backup solutions to ensure seamless operations 24/7, driving sustained market growth.

Industrial Automation and Digital Transformation: As industries adopt automation and machine-to-machine communications, uninterrupted power becomes essential for maintaining production continuity. UPS batteries are widely deployed in manufacturing, healthcare, telecommunications, and energy sectors to safeguard critical infrastructure.

Smart Grids and Infrastructure Modernization: The growing implementation of smart grids, smart meters, and automated energy systems also fuels UPS battery demand by addressing reliability gaps in power distribution networks. A backup energy source is crucial when smart systems rely on constant connectivity.

Request Free Sample Report : https://www.stellarmr.com/repo....rt/req_sample/UPS-Ba

What Lies Ahead: Emerging Trends Shaping the Future

The UPS battery market is evolving with various technological and structural trends:

Shift Toward Lithium-Ion and Advanced Chemistries: While lead-acid batteries remain widely used due to low initial cost, lithium-ion batteries are gaining traction thanks to higher energy density, longer lifespan, lower maintenance needs, and faster recharge times — especially in data centers and commercial applications.

Integration with Renewable Energy and Energy Storage Systems: As renewable energy sources like solar and wind become more prevalent, UPS batteries are increasingly integrated into broader energy storage solutions that provide both backup and optimization benefits in grid-tied setups.

Smart Monitoring and Battery Management Systems: Advanced monitoring features and battery management systems improve performance, predict failures, and optimize maintenance schedules, reducing the total cost of ownership and increasing reliability.

Demand from Emerging Markets: Rapid digital infrastructure expansion in Asia Pacific and other emerging regions is expected to reinforce market growth, driven by investments in telecommunications, industrial automation, and data center buildouts.

Segmentation Analysis from the Report

The Stellar Market Research report segments the UPS battery market as follows:

By Topology:

Online UPS — This segment dominates the market due to its continuous double-conversion design, which provides clean, uninterrupted power by always routing energy through the battery and inverter system.

Standby UPS — Often used for residential and small commercial needs due to compact design and basic surge protection.

Line Interactive UPS — Offers a balance between cost and performance, with voltage regulation and battery backup functions.

By Product Type:

Lead-Acid Batteries — Cost-effective and widely used, particularly in traditional and budget-sensitive installations.

Lithium-Ion Batteries — Growing rapidly, especially in data center and enterprise applications where lifecycle performance and energy density are valued.

Nickel Cadmium Batteries — Used for specific industrial applications requiring robust performance in challenging environments.

By Application:

Residential — Provides backup power for home electronics and small office systems.

Commercial — Utilized in office buildings, retail environments, and institutional installations.

Data Center — A key growth segment given the demand for continuous uptime and data security.

Industrial — Used in manufacturing, energy, healthcare, and other sectors requiring reliable power continuity.

By Region: Geographic segmentation includes North America, Europe, Asia Pacific, Middle East & Africa, and South America, with insights into regional demand patterns and projected growth trajectories.

Country-Level Analysis: USA and Germany

United States: The U.S. UPS battery market is strongly supported by its mature digital infrastructure, widespread adoption of data centers, and stringent reliability standards in commercial and industrial sectors. High demand for cloud services, IoT adoption, and enterprise automation drives consistent investments in UPS and backup power solutions.

Germany: As one of Europe’s leading industrial economies, Germany shows strong adoption of UPS systems — particularly in manufacturing, telecommunications, and healthcare. Increasing focus on energy reliability, industrial digitization, and renewable integration supports steady market expansion.

Both markets reflect strong commitment to infrastructure resilience and technological innovation as foundational drivers of UPS battery demand.

Commutator Analysis (Competitive Landscape)

The UPS battery market is populated by a mix of global energy storage and power electronics companies focusing on performance, reliability, and technology integration. Notable players include:

Saft Batteries

Kokam Co., Ltd.

Kehua Data Co., Ltd.

Toshiba Corporation

Socomec

Active Power

EnerSys

Vertiv

Schneider Electric

Leoch International Technology Limited

GS Yuasa Corporation

FIAMM Energy Technology S.p.A.

Exide Industries Ltd.

Eaton

East Penn Manufacturing

CSB Energy Technology Co., Ltd.

These companies compete on battery chemistry innovations, energy density improvements, longer cycle life, and integration with smart power systems.

Press Release Conclusion

The UPS Battery Market is poised for strong growth through 2032 as global reliance on digital infrastructure, data centers, automated industrial processes, and smart grids intensifies. With a projected valuation of over USD 2.1 billion by 2032 and a CAGR of approximately 9.2 %, the market reflects the increasing importance of uninterrupted power solutions across critical sectors. Advances in battery technologies — particularly lithium-ion — and diversification of UPS applications will continue to shape the competitive landscape, offering compelling opportunities for manufacturers, system integrators, and end users alike.

About us

Phase 3,Navale IT Zone, S.No. 51/2A/2,

Office No. 202, 2nd floor,

Near, Navale Brg,Narhe,

Pune, Maharashtra 411041

sales@stellarmr.com